10 Retirement Risks

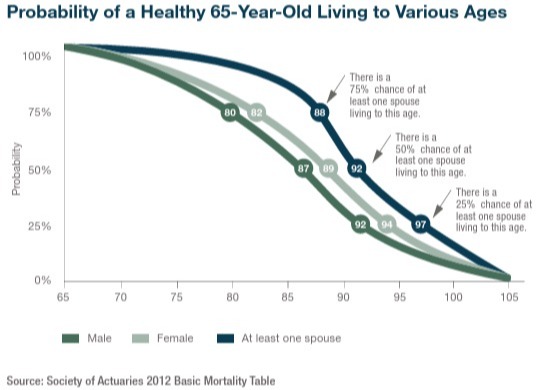

- Longevity

Longevity in retirement is the possibility of living 20, 30, or even 40 years after leaving the workforce which makes having reliable, lasting income sources more important than ever. As people live longer, they face risks like outliving their savings, rising healthcare costs, and inflation eroding purchasing power. To manage longevity risk, many retirees use a "floor and upside" approach, secure essential expenses with guaranteed income (like Social Security and annuities) and use investments for growth.

- Outliving Your Savings

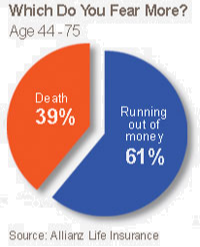

Outliving your savings is the risk of running out of money before the end of your life, leaving you financially vulnerable in retirement. This can result from living longer than expected, high expenses, poor investment returns, or withdrawing too much too soon. Inflation and market downturns also reduce purchasing power over time. To manage this risk, it’s important to save consistently, invest for long-term growth, and consider delaying retirement. Guaranteed income sources like annuities or pensions can provide lifetime payments. With a 65-year-old facing a 50% chance of living into their 90s, careful planning is essential to ensure your money lasts.

- Inflation

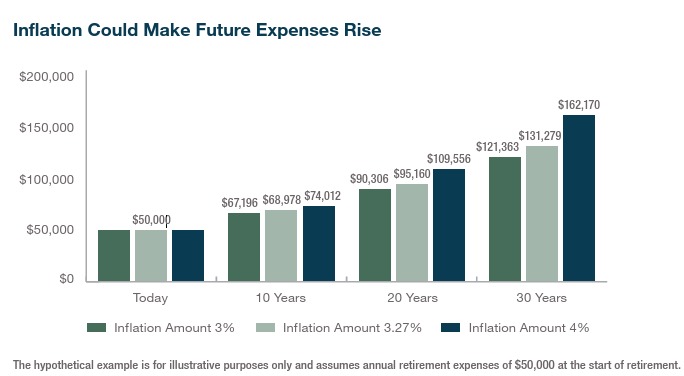

Inflation is the rate at which the general level of prices for goods and services rises over time, leading to a decrease in the purchasing power of money. In simple terms, as inflation goes up, each dollar buys less. If inflation is 5%, something that cost $100 last year would cost $105 this year. While it can’t be completely avoided, it can be managed with smart monetary, fiscal, and supply-side policies. Controlled inflation, around 2% per year, is considered healthy for a growing economy. If inflation averages 3% a year, prices double roughly every 24 years. If inflation is higher, then prices double much faster. If you have a strong base of guaranteed income, you can invest the rest of your portfolio in ways that have more risk but bring higher returns. This is a great protection against future inflation, since you may need to rely on withdrawals from your portfolio to keep up with rising costs of living over time.

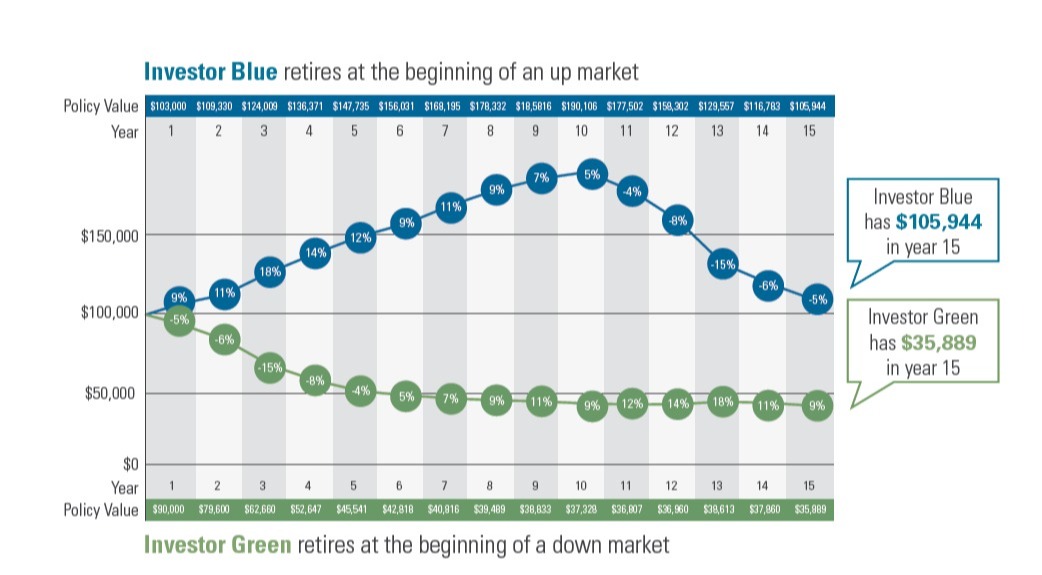

- Market Risk

Sequence of return risk is the danger that poor investment returns early in retirement, combined with regular withdrawals, can significantly reduce how long your savings last. Even if your average return is strong over time, losses at the beginning can force you to sell investments at low prices, leaving less to recover when markets rebound. This risk doesn’t affect people still saving, but it's critical for retirees drawing income. Managing it involves strategies like holding cash reserves, reducing spending during downturns, or using annuities for steady income. Timing matters just as much as the returns themselves.

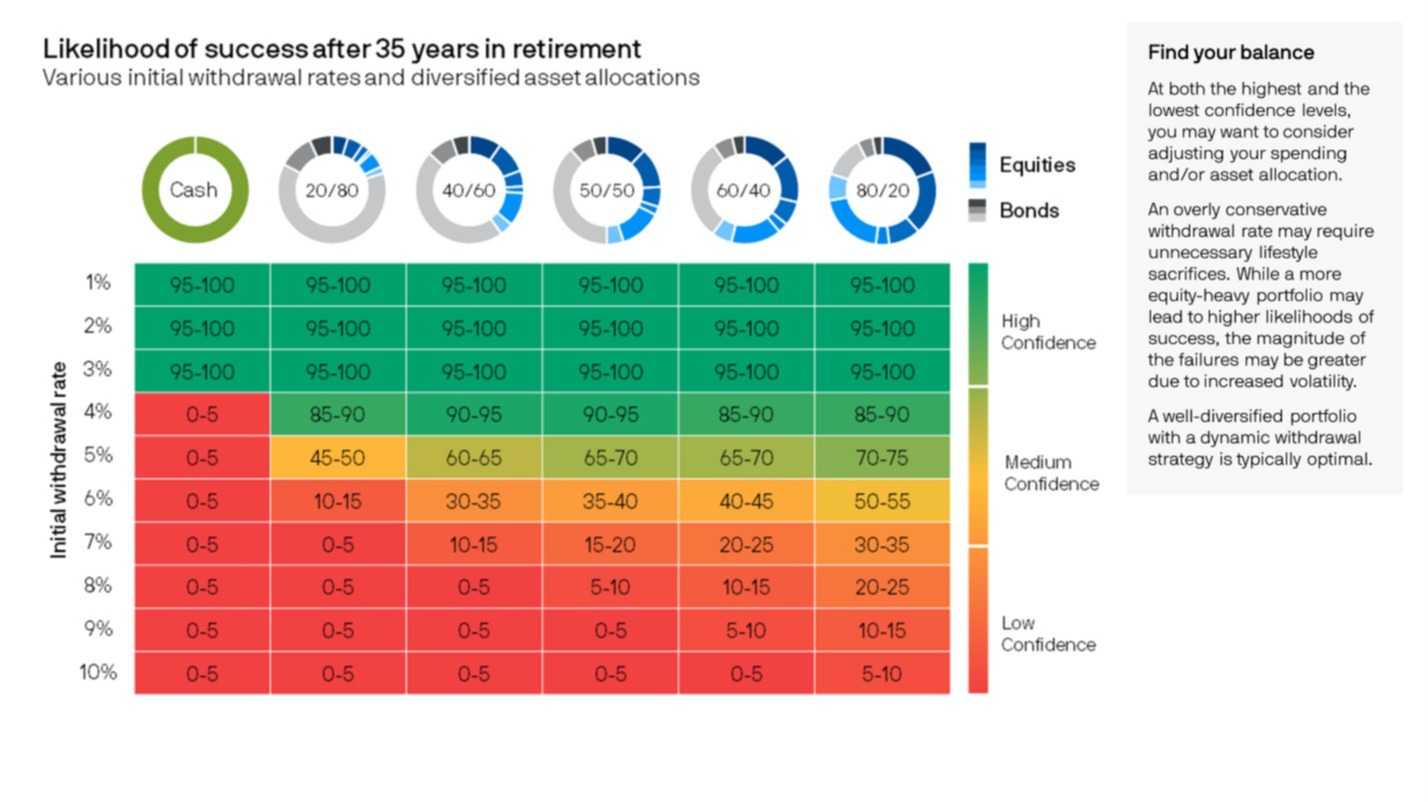

- Withdrawal Rate Risk

Withdrawal rate risk is the risk of drawing down your retirement savings too quickly, increasing the chance of running out of money later in life. This is especially dangerous if poor market returns occur early in retirement, as large withdrawals during downturns can permanently damage your portfolio. Even a small increase in the annual withdrawal rate can greatly reduce how long your money lasts. To manage this risk, many retirees use strategies like the 4% rule or adjust withdrawals based on market performance, ensuring spending aligns with the portfolio’s ability to support it over a 20–30+ year retirement.

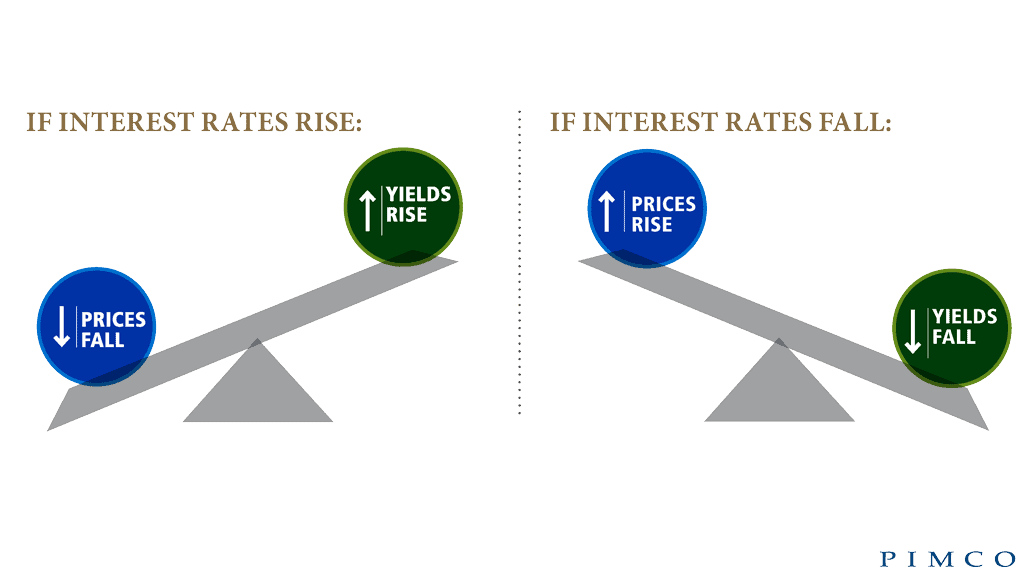

- Interest Rate Risk

Interest rate risk is the risk that changing interest rates will reduce the value of fixed-income investments like bonds. When rates rise, existing bond prices fall, which can hurt retirees relying on them for income or stability. Falling rates reduce income from new bonds and savings. This risk affects both portfolio value and cash flow. To manage it, retirees can ladder bond maturities, diversify across durations, and include inflation-protected securities (like TIPS). A balanced approach helps protect retirement income.

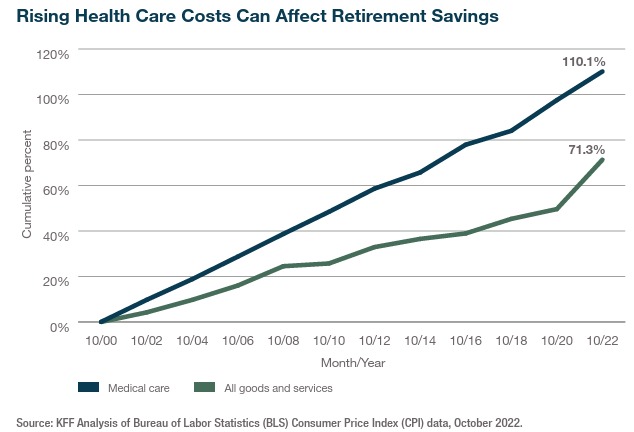

- Healthcare & Long-Term Care Risk

Healthcare and long-term care risk in retirement is the chance of facing high medical or caregiving costs that can drain savings. Medicare doesn’t cover everything, especially extended care like nursing homes or in-home assistance, which can be very expensive. Without planning, retirees may need to spend down assets or rely on Medicaid. To reduce this risk, consider long-term care insurance, build a dedicated healthcare fund, and choose Medicare and supplemental plans wisely. Planning helps protect both your finances and your independence.

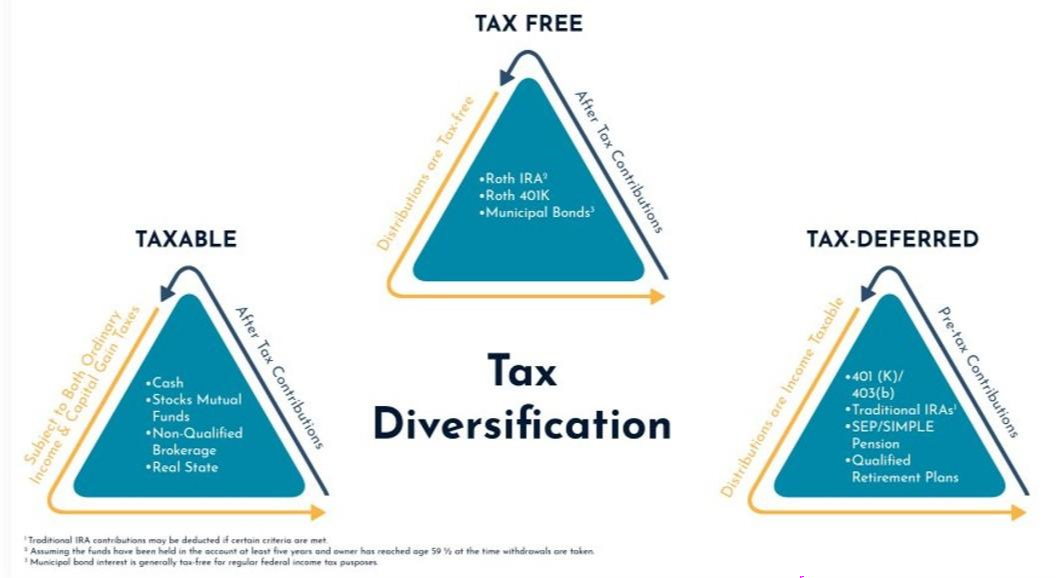

- Tax Risks

Tax risk in retirement is the possibility that taxes will significantly reduce your retirement income, especially if most of your savings are in tax-deferred accounts like traditional 401(k)s or IRAs. Withdrawals from these accounts are taxed as ordinary income and may push you into a higher tax bracket. Required Minimum Distributions (RMDs), taxable Social Security benefits, and Medicare premium surcharges can further increase your tax burden. Many retirees also face unexpected taxes from investment gains or changes in federal and state tax laws. Without careful planning, taxes can erode the value of your savings and limit your financial flexibility. To reduce this risk, it's wise to diversify account types (Roth, traditional, taxable), consider Roth conversions during low-income years, and create a tax-efficient withdrawal strategy. Staying aware of tax thresholds and working with a financial advisor can help you minimize tax surprises and preserve more of your income throughout retirement.

- Government Policy Changes

Policy and Social Security risk refers to the uncertainty surrounding future changes in government programs that many retirees rely on, particularly Social Security and Medicare. As these programs face long-term funding challenges, there is a possibility of reduced benefits, higher taxes, delayed eligibility ages, or increased costs for retirees. Because Social Security provides a significant portion of income for many retirees, even small policy changes can have a large financial impact. Additionally, shifting political priorities or budget pressures could lead to changes in healthcare coverage or tax laws that affect retirement planning. To manage this risk, retirees should avoid relying solely on government benefits and instead build personal savings, diversify income sources, and stay informed about policy developments. Having a flexible financial plan can help cushion the impact of future changes and maintain financial stability in retirement.

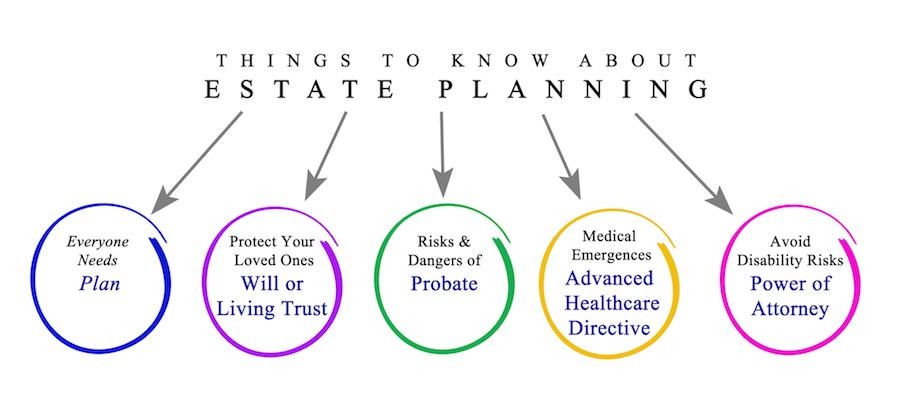

- Estate & Legacy Planning Risks

Estate and legacy planning risk is the risk that your assets won’t be passed on as intended, leading to probate delays, legal disputes, or unnecessary taxes. Without proper documents—like a will, trust, or updated beneficiary designations—your estate may be divided by default state laws. This risk also includes not planning for incapacity or failing to support dependents or charitable goals. To reduce it, create a clear estate plan, keep it updated, and communicate your wishes to family and advisors, ensuring your legacy is protected and efficiently transferred.