Cash Balance 101

Cash balance plans combine the high contribution limits of traditional defined benefit plans with the flexibility of a 401(k) plan—allowing plan sponsors the opportunity provide real-value to employees:

Reduced taxes – Corporate and personal tax savings can be significant.

Accelerated savings – Accounts grow through employer contributions and a guaranteed interest credit.

High contribution limits – Age-weighted contribution limits allow many high earners to double or triple their annual tax-deferred retirement savings.

Creditor and asset protection – Cash balance plan assets are protected from creditors in the event of bankruptcy or lawsuits.

Appeared in the March 12, 2025, print edition of the Wall Street Journal as ‘Cash Balance Plans Turbocharge Saving’.

- A cash balance plan is a type of defined benefit retirement plan where an employer contributes a set percentage of an employee's salary each year, which is then credited to their individual account and grows with a fixed interest rate that usually is equal to the yield on 30-year Treasury bonds. The CB Plan acts like a defined contribution plan with guaranteed returns, providing a stated account balance at retirement instead of a traditional pension payout based on years of service. It's often considered a "hybrid" plan combining features of both defined benefit and defined contribution plans. When participants terminate their employment, they are eligible to receive the vested portion of their account balances.

- No, everyone does not need to be included in the Cash Balance plan. The lesser of 40% of eligible employees, or 50 eligible employees, are all that are required to be covered by the Plan (with a minimum of at least two eligible employees, unless there is only one employee). So, for most smaller companies it will be 40%, and the plan sponsor can choose by job class or another criterion that suits their business goals.

With combined Federal and State income tax rates as high as 45%, the tax savings from the contributions and the subsequent earnings on these contributions can be very significant.

For example, one single contribution of $130,000 earning a tax deferred amount of 5% a year for 30 years, would be worth $561,852 at the end of 30 years. However, if the $130,000 had been taxed in the year contributed so that an “after tax” amount was invested, and if subsequent earnings on this contribution had also been taxed in each year (assuming the highest tax rates indicated above), then at the end of 30 years the total value would be only $162,937; 29% of the amount calculated above. In summary, contributing to a Cash Balance Plan can provide tremendous tax benefits.

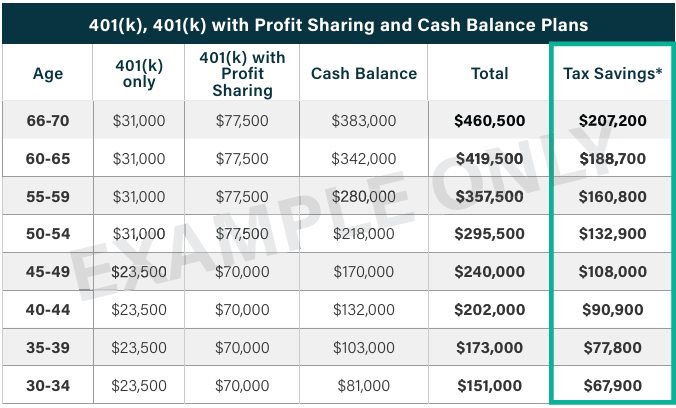

- People over age 50 typically have fewer years until retirement, therefore they can have more contributed for them by the employer every year. The employer contribution is determined by a formula specified in the plan document. It can be a percentage of pay or a flat dollar amount. Below are the limits for 2025 by age group. Below is an example of the age weighted contribution options:

- No. The “gateway contribution,” which is what this amount is called, ranges from 5% of pay to 7.5% of pay as an employer contribution (not including match) to the 401(k) profit sharing plan. Generally, if only 5% of pay is contributed, it will limit Cash Balance amounts for the owners to about $50,000 each.

- A Cash Balance plan is not appropriate if there are wide swings in profits from year-to year, if there is major uncertainty about future profits, or if the “give” (cost) to employees is too great relative to the “get” (tax deferral) for owners. Generally, Cash Balance plans are compelling when the total cost to staff is less than the tax rate paid by the owners.

- The Plan Design Illustration is what everyone gravitates toward since it is easy to understand. The visual elements help illustrate the tax-deferred retirement savings for the owners and an estimated cost to staff. To receive a free Cash Balance proposal, fill out the contact information at the bottom of the webpage.

- Funded status is an important but manageable concern. IRS rules over the last 10 to 15 years have increased the range of annual contribution from “Minimum required” to “Maximum deductible,” which gives plan sponsors more latitude to manage funding from year to year. We work with providers that have helped clients to manage through the Great Recession of 2008, the COVID pandemic of 2020, and other downturns in the market, as well as help ensure plans are not overfunded during extended bull markets.

- Sponsors normally terminate for a business reason, such as no need for the plan anymore, poor company profits, a recession, or to reduce liability to the company. Sponsors may also terminate a Cash Balance plan that’s been around many years (usually 10 or more) to allow the distribution of retirement benefits. It also provides an opportunity to set up a successor plan that is better suited to the changing demographics of the business.

- There is no stated number of years by the IRS, however, the plan needs to have some sense of permanency, and if terminated, there needs to be a good business reason for doing so. In general, 10 or more years is preferable to reduce the likelihood of IRS scrutiny about the intention of the Cash Balance plan.

- Yes and no. Yes, normally a ratio of 1:10, owner to staff, is ideal. But no, in that we’ve seen higher ratios that also make sense if the required contribution to staff employees is meaningful to them and the company.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual.

All investing involves risk including loss of principal. No strategy assures success or protects against loss.

Guarantees are based on the claims-paying ability of the PBGC/Pension Benefit Guaranty Corporation, a government agency. If a covered plan is terminated and insufficient of assets, PBGC will cover benefits up to certain legal limits.