Social Security

Social Security is a cornerstone of retirement income for millions of Americans, yet many people don’t fully understand how it works—or how to maximize their benefits. With rules that vary based on age, work history, and claiming strategy, Social Security can be more complex than it first appears. Making informed decisions about when and how to claim benefits can significantly impact your financial security in retirement. In this overview, we’ll break down the basics of Social Security, highlight key factors to consider, and help you make choices that align with your long-term retirement goals.

- Why is Social Security important?

Social Security serves as the foundation for retirement income, providing a reliable, guaranteed monthly benefit based on your earnings history to help cover essential living expenses.

- Where do you get a benefits estimate?

Go to www.ssa.gov and estimate your benefits and find other helpful information about retirement at ssa.gov/prepare/plan-retirement.

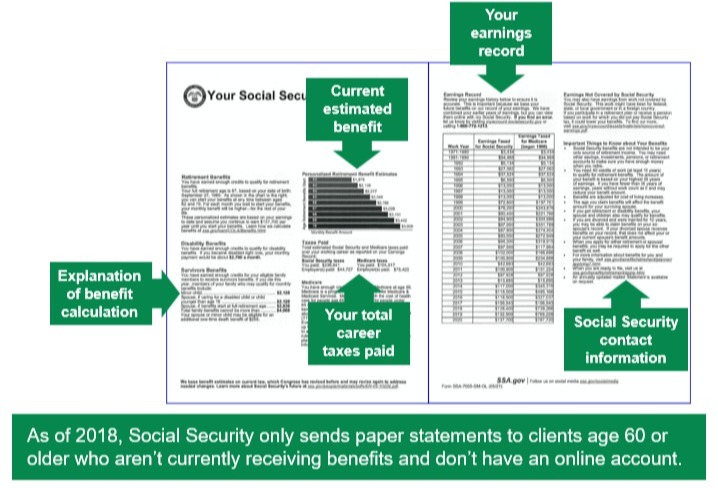

- How do I read a Social Security benefits statement?

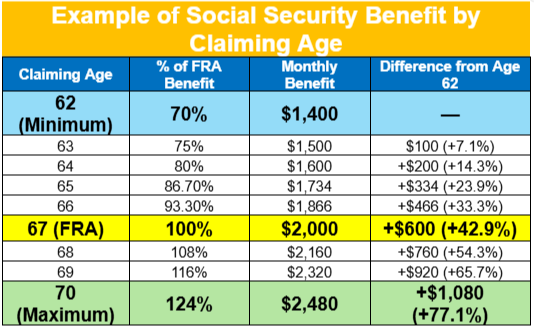

- When should I begin my benefits?

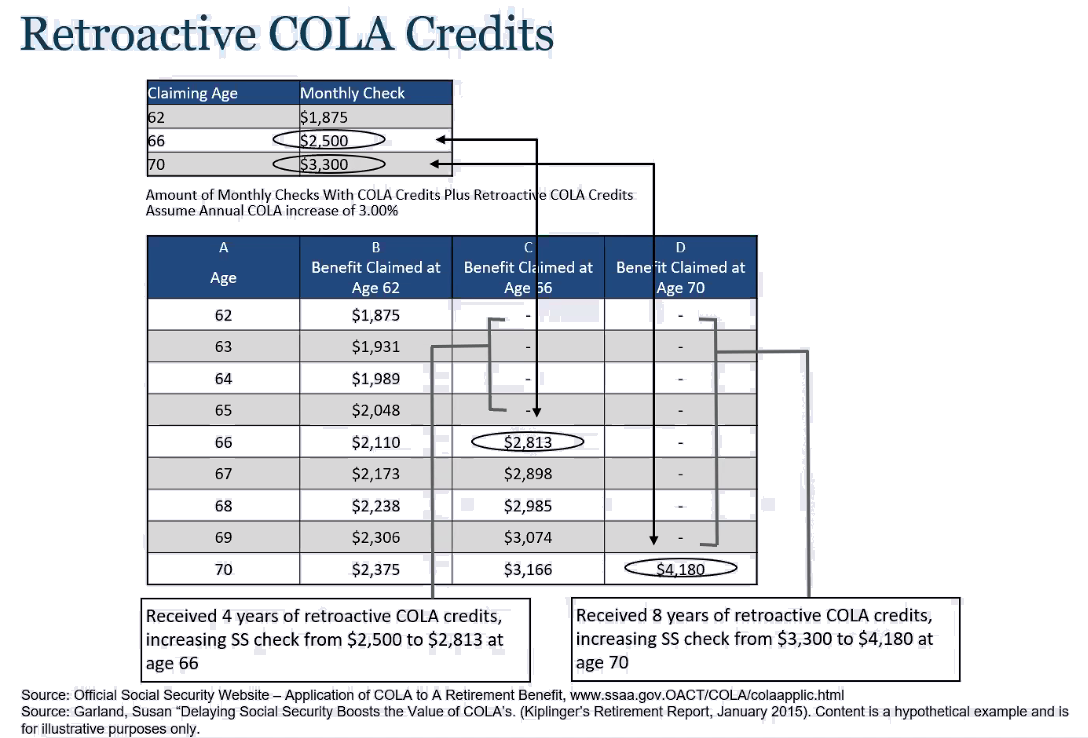

Deciding when to start your Social Security benefits depends on your health, income needs, and long-term goals. You can begin as early as age 62, but your monthly benefit will be permanently reduced up to 30% less than if you wait until your full retirement age (FRA). Waiting until full retirement age allows you to claim your full benefit, and delaying even further, up to age 70, maximizes your monthly payment by about 8% for each year you wait. Delaying may make sense if you’re in good health, have other sources of income, or want to maximize survivor benefits for a spouse. However, if you need income sooner or have health concerns, claiming earlier could be a practical choice. The right time to claim is personal—and ideally, it should align with your overall retirement income plan and is a choice of a lifetime. We can help you analyze your situation so that you make the best-informed decision for yourself. Look at the chart below as an example:

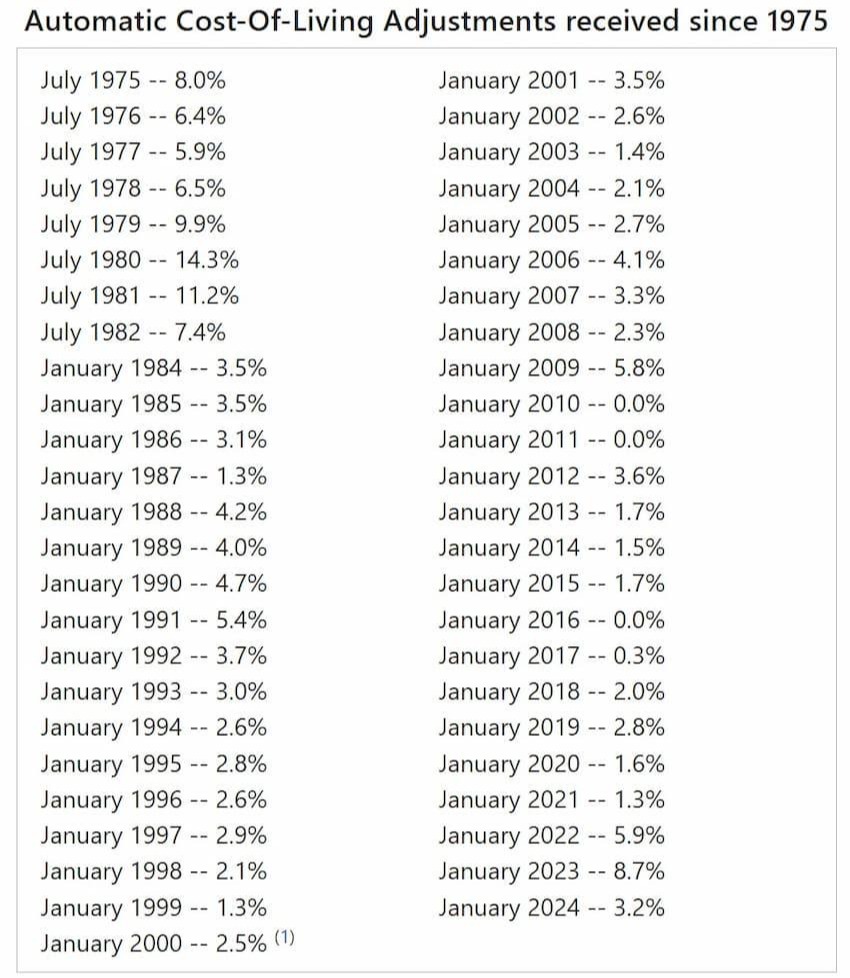

- Will my Social Security benefit ever increase?

Yes, your Social Security benefit is a lifetime benefit with annual Cost of Living Adjustments (COLA). The annual increase depends on the Consumer Pricing Index (CPI) and inflation.

- How can COLA affect my benefits claiming strategy?

- Are Social Security benefits taxed?

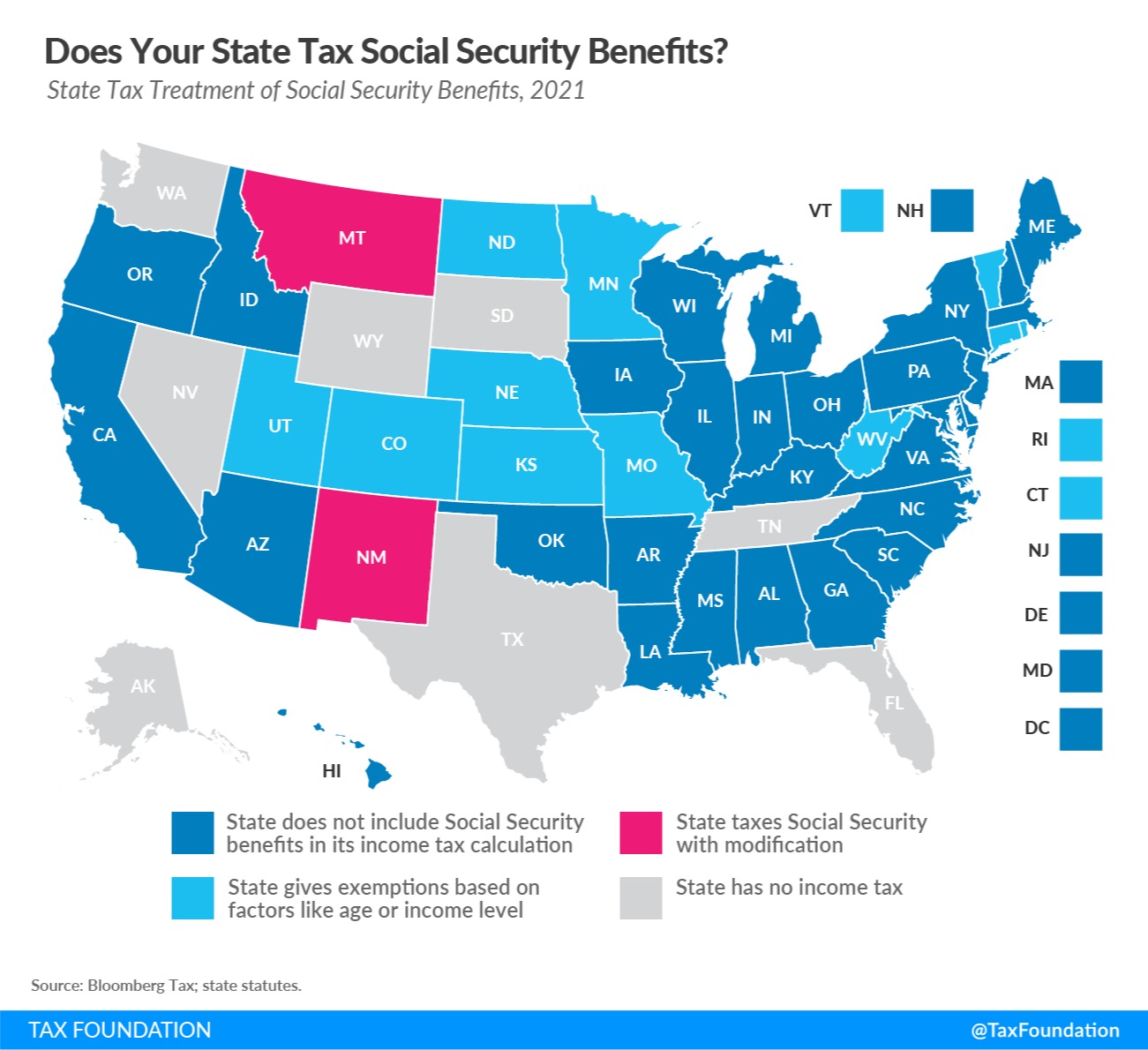

Yes, Social Security benefits can be taxed depending on your total income. The IRS uses a formula called “provisional income,” which includes your adjusted gross income, any tax-exempt interest, and half of your Social Security benefits. If you’re single and your provisional income is above $25,000—or above $32,000 for married couples filing jointly—up to 50% of your benefits may be taxable. If your income exceeds $34,000 (single) or $44,000 (married), up to 85% of your benefits could be subject to tax. However, you’ll never pay taxes on more than 85% of your Social Security benefits. Additionally, some states tax Social Security as well, though most do not. Understanding how your benefits are taxed can help you plan withdrawals from other accounts more efficiently.

- Can you work and collect Social Security at the same time?

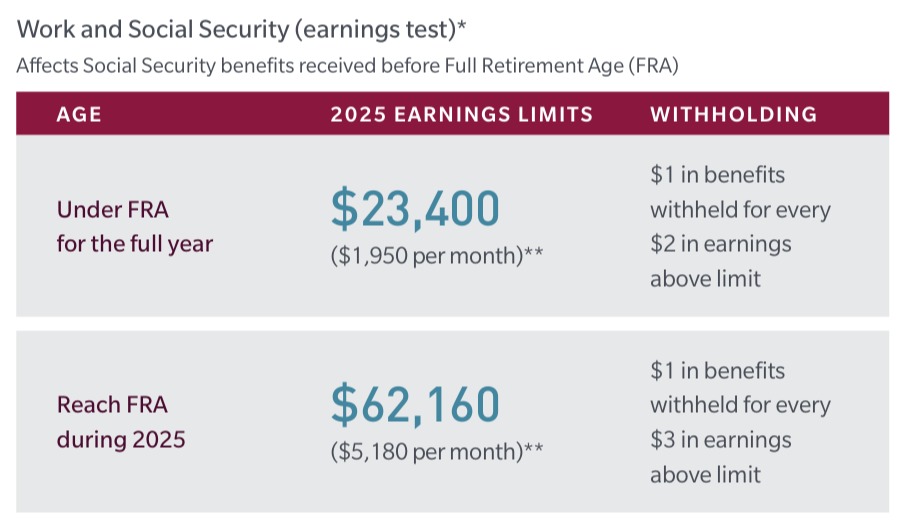

Yes, you can work and collect Social Security at the same time, but if you claim benefits before your Full Retirement Age (FRA), your benefits may be temporarily reduced based on how much you earn. In 2025, if you’re under FRA, you can earn up to $23,400 without any reduction. If you earn more, your benefits are reduced by $1 for every $2 earned above that limit. In the year you reach FRA, the limit is higher, $62,160 and the reduction is $1 for every $3 over the limit, but only for earnings before your birthday. Once you reach your FRA, you can earn any amount without a reduction in benefits, and any benefits previously withheld due to earnings will be recalculated to increase your future payments.

- What is excluded from income when calculating taxation of Social Security benefits?

- Roth IRA Distributions

- Non-Taxable Pensions and Annuities

- Qualified Charitable Distributions

- Inheritance/Gifts

- Life Insurance Proceeds

- Qualified Medical Distributions from Health Savings Accounts (HSAs)

- Will Social Security run out of money?

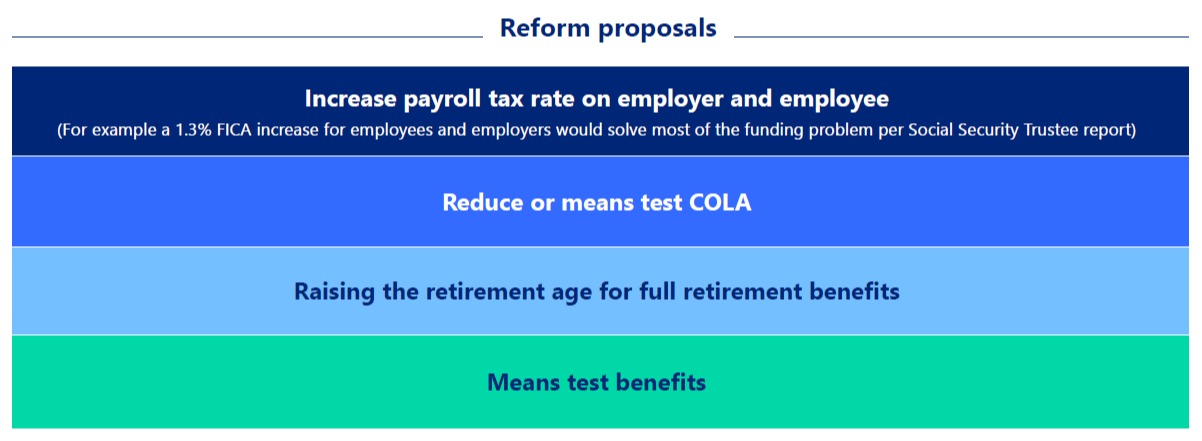

Social Security is not going away, but it is facing a funding challenge. Without any changes, the Social Security Trust Funds—which supplement payroll tax revenue—are projected to be depleted around 2034. Even then, payroll taxes will still cover about 77–80% of scheduled benefits, meaning payments would continue but at a reduced level. To avoid benefit cuts, action is needed. Potential solutions include raising payroll taxes, increasing the retirement age, adjusting benefits, or some combination of these strategies. Policymakers have proposed various reforms, typically focused on either boosting revenue, reducing costs, or blending both approaches to secure the program’s long-term stability.

- What else should you know about Social Security?

Medicare

Understanding Medicare is essential for retirees because healthcare becomes a major expense in retirement. Making informed choices helps avoid coverage gaps, late enrollment penalties, and unexpected costs. With different parts (A, B, C, and D), retirees need to understand what each covers and how it fits into their overall financial and healthcare plan. Medicare decisions also impact other areas like Social Security timing and supplemental insurance needs. Proper planning ensures better coverage, cost control, and peace of mind.

- What is Medicare?

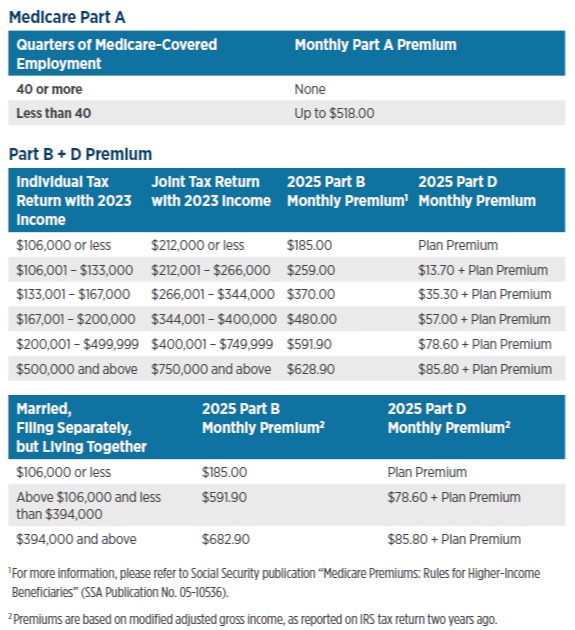

Medicare is a federal health insurance program primarily for people age 65 and older. It plays a vital role in helping retirees manage healthcare costs during retirement. Medicare is divided into parts that cover different services: Part A covers hospital care, Part B covers doctor visits and outpatient services, Part C (Medicare Advantage) offers an all-in-one alternative through private insurers, and Part D covers prescription drugs. Understanding how each part works—and what’s covered or not—can help you make informed choices about your healthcare in retirement.

- What does Medicare Part A cover?

Medicare Part A coverage was first introduced in 1965 to help seniors manage the high cost of hospital care. Part A covers hospital visits, certain hospital treatments and procedures, skilled nursing facility care (not including long-term care), and hospice care.

- What does Medicare Part B cover?

Medicare Part B covers certain health care costs not covered by Part A, such as doctor visits and services, outpatient hospital care, physical and speech therapy, lab tests, blood transfusions, medical equipment and supplies, and ambulance services. Part A and Part B together are also known as Original Medicare.

- What is Medicare Advantage (Part C)?

This coverage is an alternative to Part A, Part B, and Medigap. Medicare Advantage (which is also called Medicare Part C) is an "all-in-one" managed care plan that provides the coverage you'd find under Original Medicare and Medigap, and can also include Part D prescription drug coverage, vision coverage, or dental care.

Sounds great, right? Well, there's a catch. Medicare Advantage plans provide coverage for what's called "in-network services." Each Medicare Advantage plan works with a network of doctors and health care facilities. Most Medicare Advantage plans require a beneficiary to go through their network for services, but plans vary. For example, while HMOs provide only in-network services, PPOs have a network but allow you to go out-of-network with higher cost sharing.

- What is Medicare Part D?

Original Medicare and Medigap plans do not provide prescription drug coverage, which means you may want to purchase a Part D plan or a Medicare Advantage plan that includes prescription drug coverage. Enrolling in a Part D plan is not required. However, if you don't enroll in a Part D plan when you first become eligible, and you don't have other prescription drug coverage, you may wind up getting penalized financially by paying a late enrollment penalty for the rest of the time you maintain Medicare drug coverage, should you enroll later.

Regardless of the coverage you choose for prescription drugs, it's important to consider the ones that cover the medications you need, how often you need them, and where you purchase them.

- What is Medigap?

A Medigap policy is private health insurance that helps supplement Original Medicare. This means it helps pay some of the health care costs that Original Medicare doesn't cover (such as copayments, coinsurance, and deductibles). These are "gaps" in Medicare coverage. If you have Original Medicare and a Medigap policy, Medicare will pay its share of the Medicare-approved amounts for covered health care costs. Then your Medigap policy pays its share.

While the federal government provides Parts A and B, private health insurance companies offer Medigap plans. There's a wide variety of Medigap plans to choose from that address services you need that Parts A and B don't cover.

- Where can you find reliable Medicare information?

Medicare.gov is the official U.S. government website for Medicare, providing reliable, up-to-date information about Medicare coverage, costs, and enrollment. It serves as a central hub where individuals can compare plans, apply for benefits, manage their coverage, and learn about the different parts of Medicare—Parts A, B, C, and D.

The site also offers tools to help users estimate costs, find local providers, and review prescription drug coverage. Whether you're approaching age 65, already enrolled, or helping someone else navigate their options, Medicare.gov is a trusted resource for making informed healthcare decisions in retirement.

- What is the monthly premium of Medicare?

Pensions

Pensions were once a common part of retirement, but today they’re far less widespread. In fact, only about 13 million currently employed Americans have a defined benefit pension plan, according to the Pension Benefit Guaranty Corporation. If you're among them, it's important to consider the advantages and drawbacks of taking your pension as a lump sum or as a steady stream of income. If you don’t have a pension, you still have options—such as annuities or structured withdrawal strategies—to create a reliable, pension-like income in retirement.

Lifetime Income Solutions

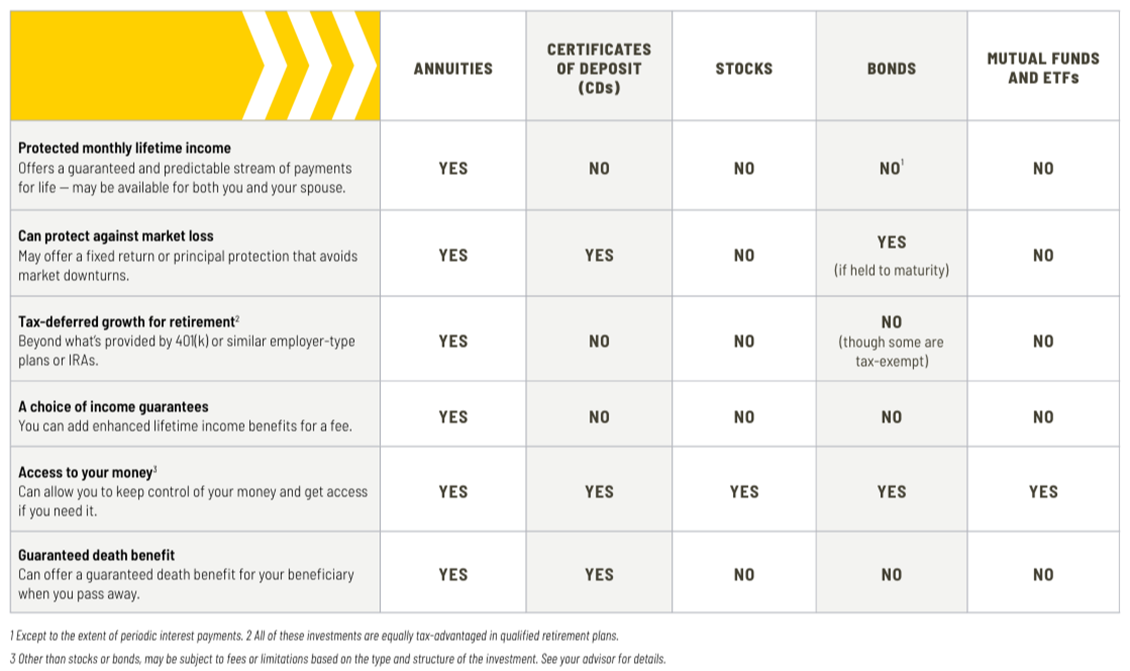

Annuities are financial products designed to provide a steady stream of income, often used as part of a retirement strategy. Offered by insurance companies, annuities can help individuals convert savings into predictable income, either for a set number of years or for life. There are several types including fixed, indexed annuities, and immediate, each with its own features, risks, and benefits. Annuities can offer tax-deferred growth, guaranteed income, and protection against outliving your money, making them an appealing option for those seeking long-term financial security in retirement.

- How can an annuity supplement my monthly income ?

Annuities can help cover monthly expenses in retirement by providing guaranteed monthly income for life similar to a pension. They can supplement Social Security and fill gaps between essential costs and other income sources. With a lifetime income annuity, you convert a lump sum into consistent monthly payments, reducing the risk of outliving your savings. This income remains stable regardless of market performance. Some annuities also offer inflation protection or spousal continuation. For example, if your expenses are $3,000 per month and Social Security provides $2,100, an annuity paying $900 ensures your basic needs are met with predictable income throughout retirement.

- How do the benefits of annuities compare to those of CDs, stocks, bonds, and mutual funds?

- What happens to my money if I die?

Most annuities allow you to name a beneficiary, who will receive any remaining balance or death benefit, depending on the contract terms.

- How do I know that the annuity company selected is safe?

All insurance companies have a rating for financial strength provided by rating agencies like A.M. Best, Standard & Poor’s, Moody’s, and Fitch. Ask your financial professional about the financial ratings of the insurance company you are considering.

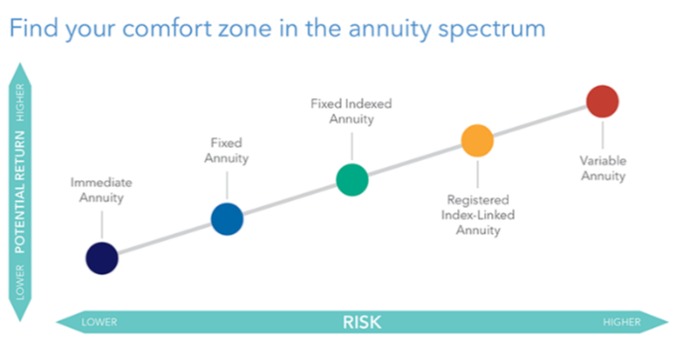

- What are differences between fixed, fixed indexed and income annuities?

Fixed Annuities

- Guaranteed interest rate and term

- Principal protection

- Similar to a Certificate of Deposit (CD)

- Tax-Deferred growth

- No contribution limits

- Avoids Probate

*Ideal for conservative clients that like CDs or want to avoid market volatility.

Fixed Indexed Annuities (FIA)

- Guaranteed Lifetime Income Option

- Principal Protection

- Tax-Deferred Growth

- Market Linked Growth Potential

- Downside Protection + Upside Market Participation

- Personal Pension, often with growth bonuses

- No Contribution Limits

- Avoids Probate

*Ideal for clients that want growth with guardrails or want to replace their paycheck in retirement after a year.

Immediate Annuities

- Guaranteed Lifetime Income Option

- Protection from Market Volatility

- Simple and Predictable

- Paycheck Replacement

- Avoids Probate

*Ideal for clients that want to replace their paycheck within a year of retirement.

- What is the missing piece of Retirement Income?

“There are only three sources of income you can count on for life: Social Security, a pension, and an annuity. Everything else is subject to market risks. An annuity could be the missing piece in your retirement security.” — Alliance for Lifetime Income

Dividend & Interest Income

Investment dividend income can play a key role in retirement by providing a steady stream of cash flow from stocks, mutual funds, or ETFs that distribute a portion of their profits to shareholders. This income can help cover regular expenses without depleting your investment principal, making it a valuable complement to Social Security and other retirement income sources as part of a multi-source retirement income strategy.

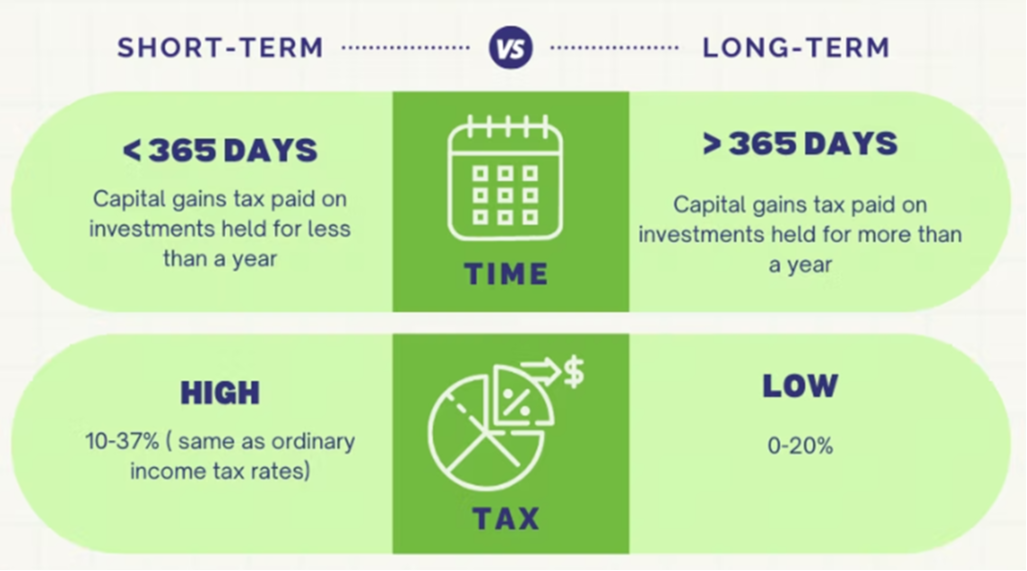

- How are capital gain taxes calculated ?

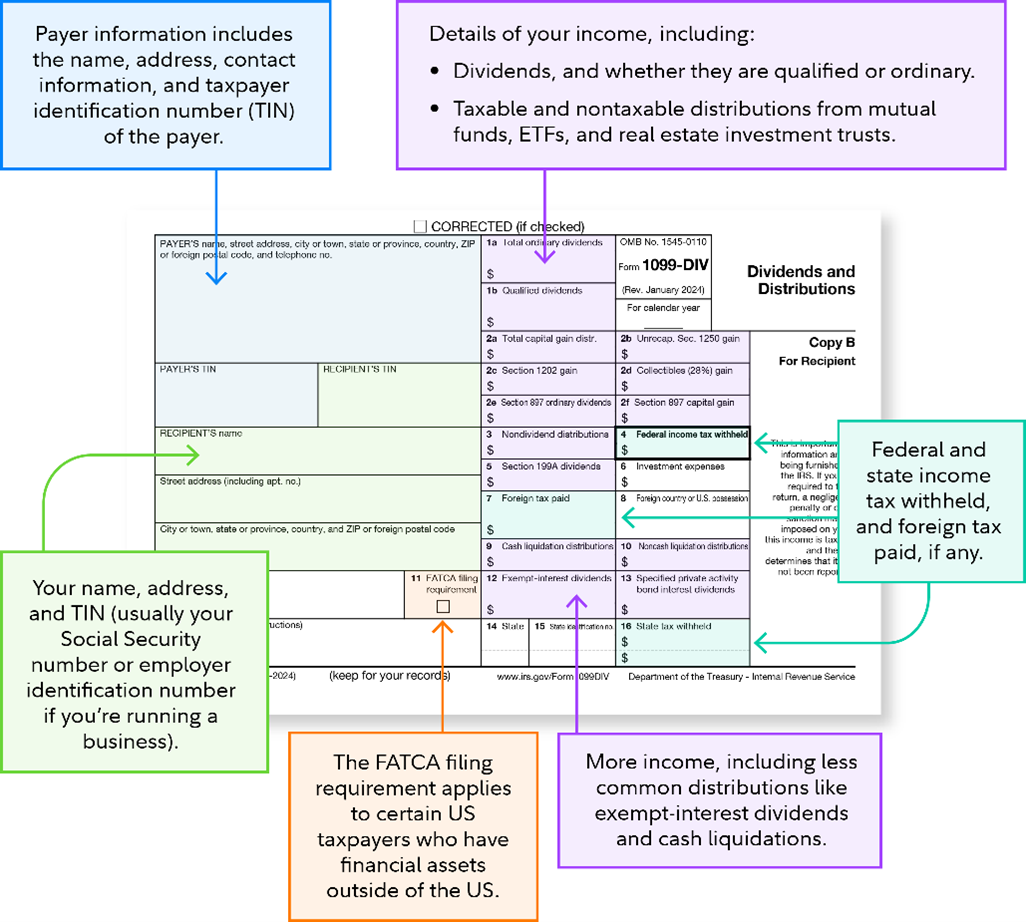

- What is the difference between Qualified vs. Ordinary dividends on 1099-DIV ?

A 1099-DIV will show if your dividends are considered qualified or ordinary. Ordinary dividends are taxed at your marginal rate, which could be as high as 37% for tax year 2024. Qualified dividends, on the other hand, are taxed at a more favorable long-term capital gains tax rate, ranging from 0% to 20%, depending on your income and tax-filing status. Higher earners are also impacted by the 3.8% net investment income tax (NIIT). Still, taxes on ordinary dividends tend to be higher than on qualified dividends.

- What is a 1099-DIV tax form?

A 1099-DIV is a tax form that reports certain kinds of investment income. It's one of many 1099 forms, all of which report income outside of employee wages. The “DIV" in 1099-DIV refers to dividend payments from stocks, or when companies distribute some of their profits to shareholders. A 1099-DIV also reports capital gains distributions from mutual funds.

- Who receives a 1099-DIV tax form?

You’ll receive a 1099-DIV if you earn at least $10 in dividends in a taxable brokerage account. Retirement accounts like 401(k)s and individual retirement accounts (IRAs) defer taxes, so investors don’t receive a 1099-DIV for dividends in these accounts.

- Who sends the 1099-DIV tax form ?

Brokers, banks, and other financial institutions prepare and send out 1099-DIV forms so investors know what income to report to the IRS. The IRS also receives a copy of each 1099-DIV to track a person's taxable investment income.

- How do I read the 1099-DIV tax form ?

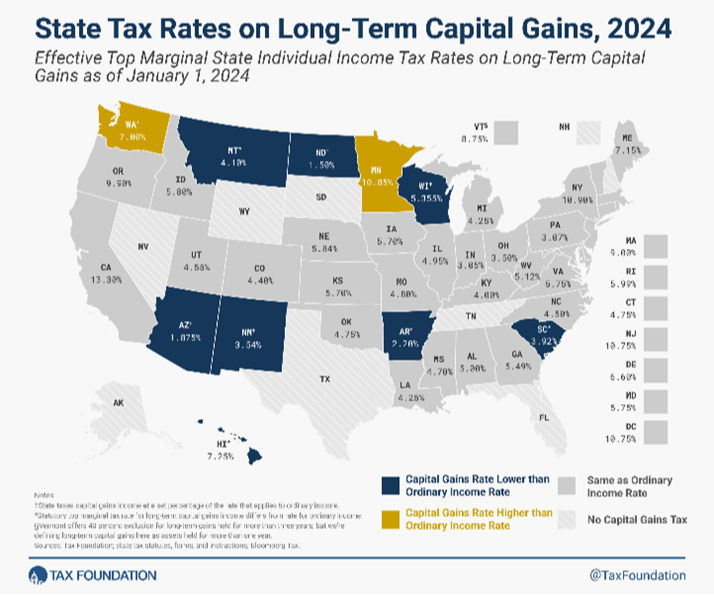

- What are the capital gains rates for state income taxes ?

Estate & Legacy Planning

Estate planning is the process of organizing your legal, financial, and personal affairs to ensure that your assets are managed and distributed according to your wishes in the event of your death or incapacity. It includes tools like wills, trusts, powers of attorney, healthcare directives, and tax strategies. All of which are designed to protect your family, avoid probate, and preserve your wealth.

- What is the difference between Estate and Legacy Planning?

Estate planning is the process of organizing the transfer of your assets after death. It typically involves creating legal documents such as wills, trusts, powers of attorney, and healthcare directives. The main goals are to ensure your property is distributed according to your wishes, reduce estate taxes, avoid probate, and provide clear guidance for loved ones during difficult times.

Legacy planning, while it includes all aspects of estate planning, goes beyond just the financial and legal considerations. It focuses on the values, beliefs, stories, and life lessons you want to pass on to future generations. This might involve creating charitable foundations, writing ethical wills, sharing family history, or outlining how you hope your family continues to support causes that matter to you.

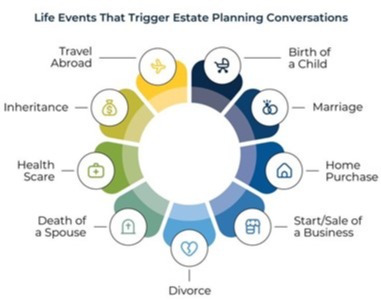

- When do most people think about estate planning?

Estate planning is often prompted by major life changes. Key triggers include marriage, divorce, or the birth of a child, which require updates to beneficiaries and guardianship plans. Purchasing or selling a home, receiving a large inheritance, or experiencing a significant increase in wealth also call for estate revisions. Starting, selling, or passing on a business adds complexity that planning can help manage. Health events, disability, or a serious diagnosis make it essential to establish powers of attorney and healthcare directives. Retirement and the death of a loved one often prompt people to revisit and refine their estate plans to ensure their wishes are clearly documented and legally protected.

- What happens without an estate plan?

Without an estate plan, your family may face unnecessary legal complications, delays, and costs. Estate planning helps:

- Protect your loved ones from uncertainty and court battles

- Ensure your business or property is handled according to your wishes

- Reduce taxes and preserve more of your wealth for heirs

- Make healthcare and financial decisions easier for your family in a crisis

- What are the common documents for estate planning?

Will

A legal document that outlines how your assets should be distributed and names guardians for minor children.Trust

A legal entity that holds assets and allows for more control, privacy, and potentially reduced estate taxes or probate delays.Power of Attorney (POA)

Authorizes someone you trust to make financial or legal decisions if you're unable to do so.Healthcare Directive / Living Will

Specifies your medical care preferences and designates someone to make healthcare decisions on your behalf.Beneficiary Designations

Ensures that accounts like life insurance, IRAs, or 401(k)s go directly to chosen individuals, bypassing probate.Letter of Intent

A non-legal document that shares personal wishes, guidance, or messages for your family or executor.Estate Tax Planning

Strategies to reduce potential federal or state estate taxes, especially for high-net-worth estates.Asset Protection

Tools to shield your estate from creditors, lawsuits, or other financial risks. - Why use an estate planning attorney?

An estate planning attorney brings legal expertise, personalized guidance, and peace of mind to one of the most important decisions you'll ever make—how to protect and pass on your legacy. While DIY solutions may seem cheaper, an attorney can help you avoid costly mistakes and give you lasting confidence that your wishes will be honored exactly as intended.

- What if I don’t want to use an estate planning attorney?

If you don’t want to use an estate planning attorney, you can still create a valid estate plan using online platforms or DIY resources, as long as you're careful and informed. These services walk you through creating wills, trusts, powers of attorney, and healthcare directives. If your situation is straightforward (e.g., no complex assets, blended families, or business interests), a DIY plan may be enough to cover your wishes legally and provide peace of mind.

Using Trust & Will offers a modern, affordable, and convenient way to create essential estate planning documents online. Trust & Will simplifies estate planning with an intuitive online platform, allowing you to create wills, trusts, and other documents from home with no office visits or legal jargon required. All documents are customized to your state laws and reviewed by legal experts, ensuring they meet legal standards and hold up in court. Traditional estate planning can cost thousands and take weeks. Trust & Will offers plans starting around $159–$599, with most people completing everything in under an hour. You get access to customer support, an estate planning attorney (if necessary, at an additional cost), updates, and even the ability to make changes over time that are helpful when life changes like marriage, kids, or homeownership occur. Ask your financial advisor about this option to get a discount on the published rate.

Retirement Milestones

Planning for retirement involves more than just choosing a date to stop working—it also means being aware of key age-based milestones that affect your benefits, taxes, and financial decisions. Important ages like 50, 59½, 62, 65, 67, and 73 each bring new opportunities, choices, or requirements related to retirement savings, Social Security, Medicare, and required minimum distributions (RMDs). Understanding these milestones helps ensure you're taking the right steps at the right time to optimize your income, avoid penalties, and maintain financial stability throughout retirement. In this section, we’ll walk through the most critical retirement age milestones and what they mean for your planning.