ESOP

Employee Stock Ownership Plans, or ESOPs, are a type of equity financing that allows employees to own shares in the company they work for. ESOPs can increase motivation and productivity, improve retention, and provide financial independence in retirement. However, there are different types of ESOPs with each one serving a specific purpose.

Unlike older Stock Bonus Plans (in place since 1921), ESOPs—created under federal law in 1974—can be “leveraged.” This means they can borrow money to buy a large block of stock, not just acquire shares gradually year by year.

ESOPs Today

- About 22,000 companies in the U.S. have ESOPs.

- Over 14 million employees participate.

- ESOPs hold an estimated $1.4 trillion in assets, representing roughly a quarter of the 401(k) market.

Types of ESOPs

Companies can design ESOPs in different ways to reward employees, fund growth, or align interests between staff and shareholders. Here are the most common types:1. Employee Stock Option Scheme (ESOS)

The most common type of ESOP, an ESOS gives employees the right to buy company shares at a set price (often below market value).

- Granted as part of a compensation package

- Subject to performance goals and vesting periods

- Once exercised, employees gain full shareholder rights (voting, dividends)

2. Employee Stock Purchase Plan (ESPP)

An ESPP allows employees to purchase company stock at a discount, often through payroll deductions.

- Builds ownership gradually over time

- Provides dividends and profit participation

- Low-risk way to invest in company growth

3. Restricted Stock Units (RSUs)

RSUs give employees the right to receive company shares once vesting conditions are met.

- Based on tenure or performance milestones

- Shares delivered after vesting

- No voting rights or dividends until vesting completes

4. Restricted Stock Awards (RSAs)

RSAs grant actual shares immediately, but with restrictions until vesting requirements are met.

- May include conditions such as performance goals or time-based vesting

- Unlike RSUs, employees technically own the shares right away, but with limits on selling or transferring them

5. Stock Appreciation Rights (SARs)

SARs provide employees with the value of stock price increases over time, usually paid in cash or shares.

- No need to purchase shares

- Rewards stock growth without downside risk

- Commonly used for executives and key employees

6. Phantom Equity Plan (PEP)

PEPs mimic stock ownership without issuing actual shares.

- Employees receive “phantom stock” tied to company performance

- Paid out in cash based on share value appreciation

- Offers equity-like rewards without diluting ownership

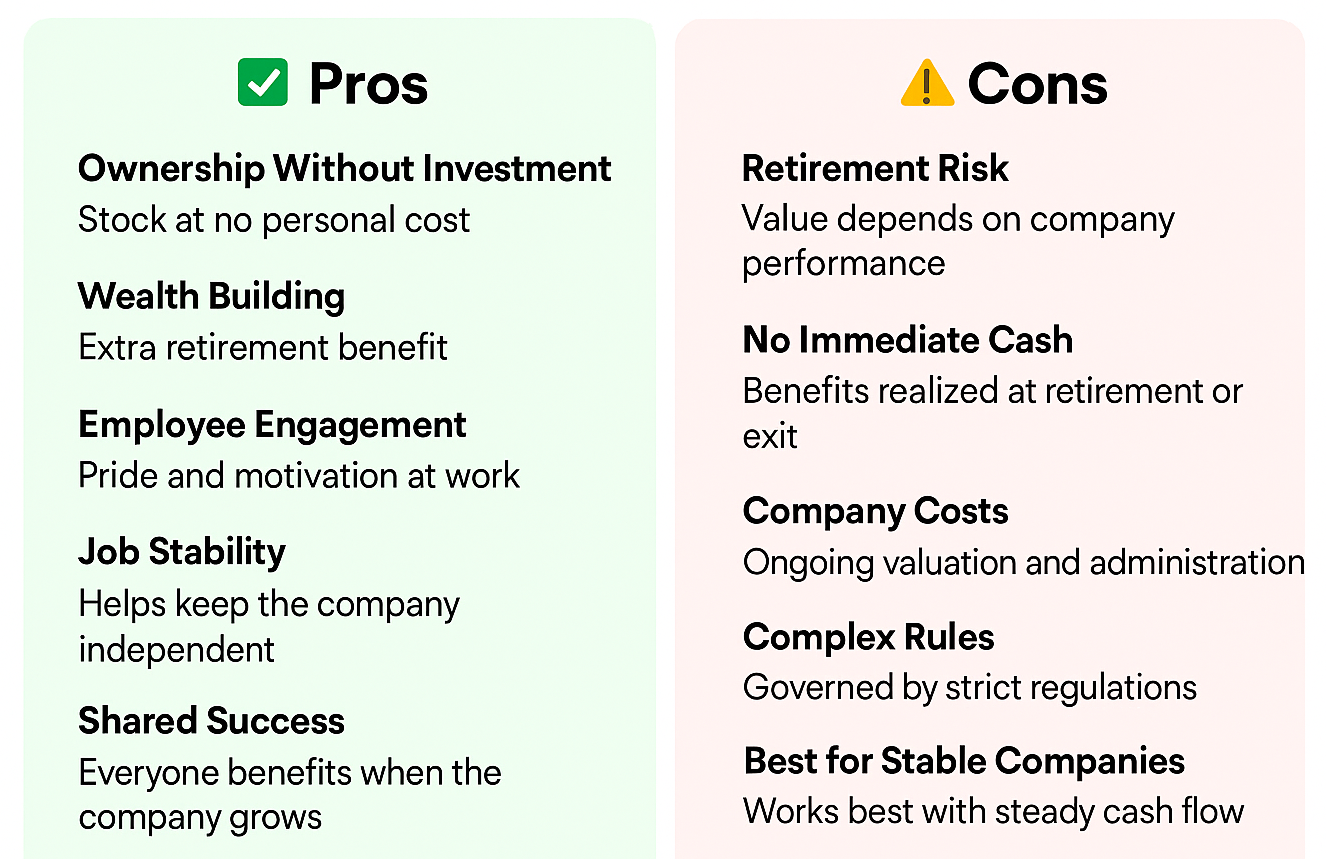

An Employee Stock Ownership Plan (ESOP) offers unique tax and financial benefits that other buyout options—like mergers or sales—cannot match.

Key Advantages

- Capital Gains Deferral (Section 1042):

If the ESOP buys 30% or more of a privately held company’s stock, the seller can defer capital gains taxes indefinitely by reinvesting the proceeds in qualified replacement property within 12 months. - Flexible Sale Options:

Unlike a merger or sale that usually requires selling 100% of the company, an ESOP allows owners to sell any portion of their shares while maintaining control until retirement. - Tax-Deductible Repayments:

Companies can use tax-deductible dollars to repay ESOP-related debt, reducing the cost of financing. - Deductible Dividends:

Dividends on ESOP stock are tax-deductible if they are either passed through to participants or used to pay ESOP loan obligations. - S Corporation Advantage:

An ESOP’s share of S corporation earnings is not subject to federal or state corporate taxes (with limited exceptions). In a 100% ESOP-owned S corporation, company earnings can be entirely tax-exempt. - Business Continuity & Legacy:

Owners can gradually transition control to key employees, preserving the company’s culture, identity, and independence instead of becoming a division of a larger firm. - Employee Attraction & Retention:

ESOPs help recruit, motivate, and retain employees by giving them a vested ownership interest. - Proven Performance Boost:

Studies show that ESOP-owned companies are often more productive and profitable than similar non-ESOP firms. - Acquisition Power:

Companies can use ESOPs to acquire other businesses with tax-deductible dollars, while sellers may qualify for tax-free proceeds under Section 1042.

- Capital Gains Deferral (Section 1042):

An Employee Stock Ownership Plan (ESOP) can provide powerful advantages for both business owners and employees:

- Owner Transition: Allows the company to buy out current owners using tax-deductible contributions.

- Employee Ownership: Gives employees a direct stake in the company’s success, sharing in both current and future growth.

- Stronger Incentives: Creates a more effective and motivating employee benefit than many traditional incentive plans.

- Retirement Value: While focused on company stock, ESOPs can also diversify investments, making them a strong long-term retirement asset.

An Employee Stock Ownership Plan (ESOP) may be a great fit for business owners who want to:

- Convert some or all of their equity into cash without giving up control or bringing in outside investors.

- Increase company cash flow and working capital.

- Boost employee motivation and productivity.

Typical Business Profile

ESOPs can work for companies in many industries—service, retail, distribution, and manufacturing. Good candidates usually have:- Pretax income of at least $200,000

- At least 7 employees (C corporation) or 12 employees (S corporation)

- Entity type flexibility – Partnerships, LLCs, and others can set up ESOPs, but must convert to an S or C corporation before selling shares to the ESOP.

Essential Components of an ESOP

To establish and maintain a successful ESOP, businesses need:

- Financial and technical plan design

- Legal documentation

- Independent valuation

- Clear employee communication

- Year-to-year administration

- Ongoing coordination with the company’s advisors

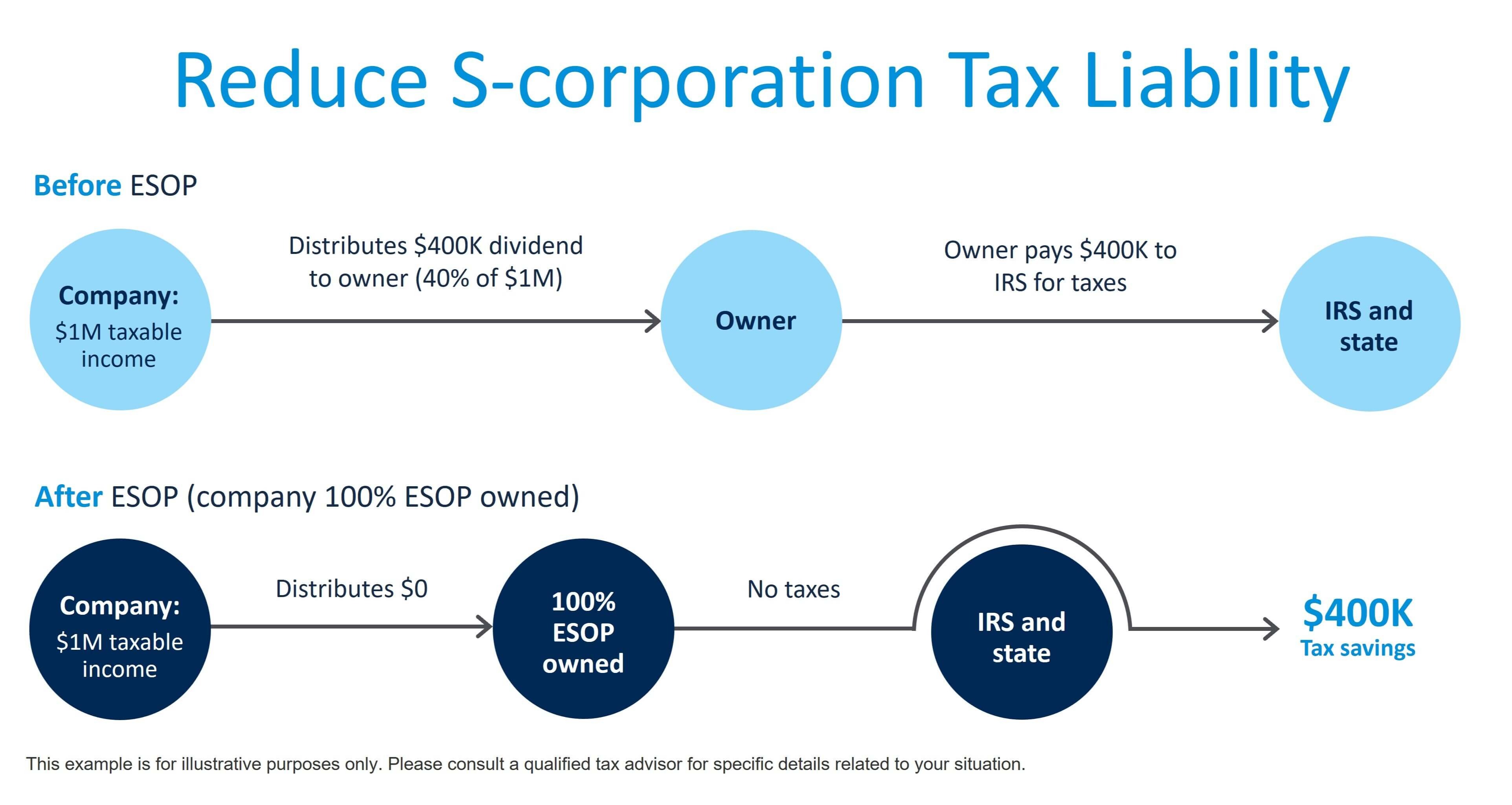

An Employee Stock Ownership Plan (ESOP) can significantly reduce an S corporation’s tax liability because the ESOP trust is a tax-exempt entity. When an ESOP owns shares of an S corporation, the percentage of company income attributable to those shares is not subject to federal income tax. For example, if the ESOP owns 100% of the company, no federal income tax is paid on the business’s profits, allowing more cash flow to be reinvested in growth, debt repayment, or employee benefits

The most common method of funding an ESOP is via an ESOP loan. The ESOP Trust purchases company stock directly from the company or individual shareholders by issuing a promissory note. The notes often have terms of 30, 50, 75, and even 100+ years. The company stock is placed in a special non-allocated account within the ESOP Trust called a suspense account. The company makes cash contributions to the ESOP Trust over the term of the note for the purpose of repaying the ESOP Trust’s loan. When a payment is made, a portion of the company stock is released from the suspense account and allocated to participants’ accounts (based on the allocation formula described in the plan document). This continues on an annual basis until the note is repaid.

Funding an ESOP via an ESOP loan has two primary purposes. First, it allows for company stock to be allocated to participant accounts over a period of time instead of all at once. This is important because after company stock is allocated, the value of that stock will eventually need to be distributed to participants at some point after they leave the company. Allocating company stock over a period of time allows the company time to plan for and manage its future distribution and diversification obligations (commonly referred to as “repurchase obligation”). Second, it keeps a pool of company stock available for future ESOP participants until the note is repaid.