Multiple Employer Plan

- What is a Multiple Employer Plan (MEP)?

A Multiple Employer Plan (MEP) is a type of retirement plan that allows two or more unrelated employers to participate in a single, shared 401(k) plan. Instead of each business setting up and managing its own plan, all participating employers pool their resources under one plan document. A MEP has been around for decades and typically requires participating employers to have a common bond, such as belonging to the same trade association, chamber of commerce, industry group, or geographic area.

Key points about MEPs:

- Shared structure: Employers join a single plan, which reduces administrative work, compliance testing, and overall costs.

- Common bond: Traditionally, participating employers must have a connection, such as being part of the same trade association, professional group, or geographic area.

- Fiduciary support: The plan sponsor (often an association or organization) assumes much of the fiduciary responsibility, lessening the burden on individual employers.

- Economies of scale: Combining assets can lead to better investment options and lower fees for participants.

- What is a Pooled Employer Plan (PEP)?

A Pooled Employer Plan (PEP) is a type of 401(k) retirement plan created by the SECURE Act of 2019 that allows multiple unrelated employers to join together in one professionally managed plan.

Key points:

- No common bond required: Unlike MEPs, businesses don’t need to share an industry, trade group, or location.

- Managed by a Pooled Plan Provider (PPP): The PPP handles most administrative, compliance, and fiduciary responsibilities.

- Cost-efficient: Pooling resources can reduce fees and improve access to investment options.

- Simplifies plan management: Employers can offer a competitive retirement benefit without the heavy administrative and compliance workload.

- What employers might benefit from a MEP or PEP?

- Employers that want to start offering a retirement plan but want to limit the expense, fiduciary liability, and time it takes.

- Employers that currently sponsor a plan and want to reduce expenses or outsource fiduciary responsibilities to an expert.

- Employers that want a turnkey solution that doesn’t require custom documents, custom plan features and provides more time to focus on running the business.

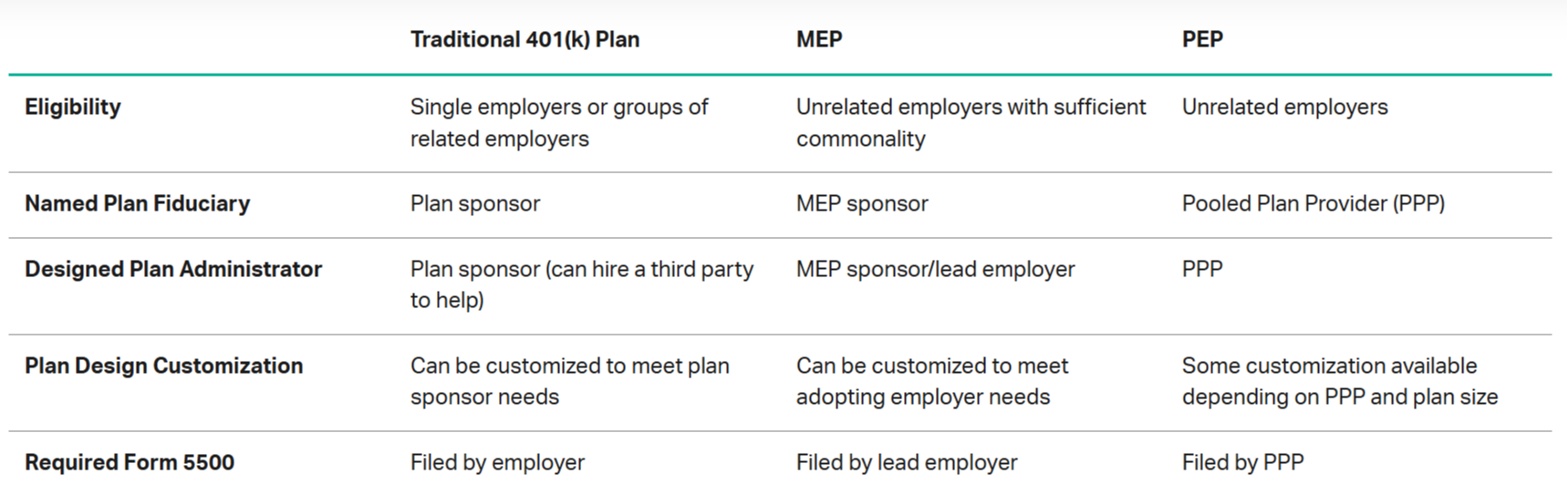

- Traditional 401(k) vs. MEP vs. PEP

- What benefits of MEP and PEP providers do we recommend for employers to do business with?

We look for providers that can:

- Integrate 402(a) named fiduciary and 3(16) administrative fiduciary, helping minimize fiduciary risk for plan sponsors

- Integrate 3(38) investment management to select and monitor the investments in the plan

- Integrate trust and custody services

- Provide payroll contribution tracking and integration

- Provide digital access to all plan functions and information

- Have the potential to integrate nonqualified plans

- What benefits of MEP and PEP providers do we recommend for employees to do business with?

We look for providers that have:

- Easy-to-use website and call center support

- Spanish-language website

- Spanish-speaking call center representatives

- Full suite of participant educational materials

- Financial wellness program

- Integrated managed account service